The world of financial markets and investments is rife with risk and reward. This is particularly true for hedge funds, sophisticated investment vehicles that are typically used only by experienced investors and firms. They are named for the fact that investors‘hedge,’ or attempt to protect their funds against volatile swings in the markets. But how are these portfolios managed? And are managers protecting and optimizing these funds as well as they should be? Seth Berlin, Principal Strategist at Performance Thinking & Technologies, a company that helps asset managers with investment operations, recently tackled these questions when working with a hedge fundclient. With the help of Palisade’s @RISK and RISKOptimizer software, Berlin was able to create a quantitative model that uses simulation to optimize a hedge fund’s portfolio.

Finding the Sweet Spot

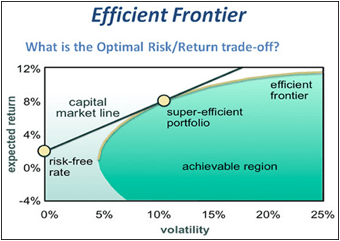

When managing a hedge fund portfolio, Berlin says, there has to be a balance between maximizing profit and minimizing risk. Modern portfolio management is based on the capital asset pricing model (CAPM). In CAPM, “You theoretically can maximize return by maximizing risk.” While taking on high risk can lead to high returns over the long term, “over the short term you would have large swings in your portfolio,” says Berlin. “Everyone can maximize profits but in the end you’re dead,” meaning some level of short-term stability is necessary.

The key, Berlin says, is to find an optimal portfolio that “maximizes return with the lowest incremental change in risk,” a sweet spot that avoids exorbitant risk while still yielding satisfactory returns. In his model, Berlin was simulating changes in capital markets assumptions and adjusting a mix of hedges to identify an optimal portfolio.

The Long and the Short of It

Berlin’s client dealt with a hedge fund portfolio comprising both long and short positions. Long positions are assets that are owned by the fund, such as stocks, which investors hope will increase in value. Short positions are ‘borrowed assets’ sold short, which increase in value if the price of the underlying assets goes down. Hedge funds use combinations of long and short positions to protect against equity market movements, currency rate changes, interest rate risk, and credit worthiness. “I’ve worked with many hedge fund managers on how they manage hedges. Anytime you can move to more quantitative than qualitative management based on simulation and optimization, it’s a win for both managers and investors.”

Turning an Art into Science

Berlin used Palisade’s risk analysis software, including @RISK and RISKOptimizer, to prove to his clients that quantitative measures of simulation could help identify an optimal portfolio, rather than the typical qualitative approach. He used a step-wise process to develop his quantitative model:

- Determine hedge ratios and constraints

- Determine decision variables to be modeled

- Determine uncertain inputs

- Model uncertain inputs using @RISK

- Output dependent on decision variables using RISKOptimizer

Simulations and Smarts

After going through this five-step process, Berlin had results that indicated how the hedge fund managers could change their profitability by altering the mix of long and short positions in the portfolio. “RISKOptimizer gave me an optimal mix of my short positions for the next week. Since this is theoretical, you then compare your results with what really happened in the next week,” he says.

These results are helpful, but of course, they are not the only answer. “I’m not an alchemist. I’m not coming up with a secret sauce that is the model for managers to make money,” says Berlin. “What I was trying to do overall is to move from a qualitative to a quantitative way to judge a problem.” He explains that managing a hedge fund will always require qualitative decisions– “that’s what experience is”–but that well done simulations provide a method to test one’s intuition and judgment.

An Underused Tool

This method Berlin used has broad applications, and could be used by anyone hedging a portfolio. Yet the majority of investors don’t apply such rigorous tests. “I think everyone would say they’re doing some kind of modeling, but for the most part it doesn’t involve simulation and optimization.” Berlin believes turning to a tool like RISKOptimizer can give some certainty and structure to the process. “Based on your capital market inputs, RISKOptimizer helps you look at different mixes of assets to reach a better risk-return structure,” he says. “If I have fifty things I want to allocate money to, and I have choices on how to allocate it, you never know the right mix. RISKOptimizer and @RISK shuffle the deck a million times, and let you see how all those different combinations could play out.”

» @RISK

» RISKOptimizer