The objective of this article is to evaluate different techniques for time series forecasting. These techniques include OLS model, Co-integration model and ARIMAX model

- Business problem: To forecast the different components of PPNR. These components include Non-interest Income and Non-interest Expense.

- Proposed solution

| OLSModel | Co-IntModel | ARIMAXModel | Notes | |

| Preference | High | Medium | Low | |

| Complexity | Low | Medium | High | |

| Dependent variable is stationary | OLS should be used | ARIMAX should be used | For ARIMAX both (dependent and independent variables) should be stationary together | |

| Independent variable is stationary | ||||

| Dependent variable is non-stationary | Co-Int should be used | ARIMAX should be used | For ARIMAX both (dependent and independent variables) should be non-stationary together | |

| Independent variable is non-stationary | ||||

| Auto-correlation | DW test close to 2 | DW test close to 2 | DW test close to 2 | If for OLS or Co-integration DW fails then ARIMAX should be used |

| Variable significance | p-value < 0.05 | p-value < 0.05 | p-value < 0.05 | For ARIMAX the AR, MA and exogenous terms should be significant |

| Multi co-linearity | VIF < 5 | VIF < 5 | VIF < 5 | |

| Residual is stationary | ADF test should pass | ADF test should pass | ADF test should pass | |

| Residual is non-stationary | For all the three approaches, the residual should be stationary | |||

| Normality and homoscedasticity of residual | Should pass | Should pass | Should pass |

- OLS

- Advantages – easy to develop / test and easy to explain

- Disadvantages– difficult to finding strong correlation between dependent and independent variables

- Co-Integration

- Advantages – easy to find strong correlations between dependent and independent variables

- Disadvantages – difficult to pass all the tests / assumptions of co-integration

- ARIMAX

- Advantages – very powerful modeling technique to overcome the shortcomings of OLS and co-integration models

- Disadvantages – complex to develop as there are two stages. In stage 1 OLS model is developed and in stage 2 ARIMAX model is developed post identification of AR and MA terms

- Introduction

- PPNR

- Pre-provision net revenue (PPNR), under the Federal Reserve’s Comprehensive Capital Analysis and Review (CCAR), measures net revenue forecast from asset-liability spreads and non-trading fees of banks.

- Pre-provision Net Revenue (PPNR) = Net Interest Income + Non-interest Income – Non-interest Expense

- Interest Income: Loans and Securities

- Interest Expense: Deposits and Bonds

- Non-Interest Income: Credit Related Fees and Non-Credit Related

- Non-Interest Expense: Employee Compensation, Processing / Software, Occupancy, Credit / Collections and Residential Mortgage Repurchase

2.2 Modeling Approaches

- If the dependent and independent variables are stationary

- ADF test is done on the independent variables. Only those variables are kept, those are stationary.

- Correlation between independent variables and dependent variable is done. Only those variables are kept, those have high correlation with dependent variable.

- OLS Model is developed.

- If the dependent and independent variables are non-stationary

- ADF test is done on the independent variables. Only those variables are kept, those are non-stationary

- Co-integration between independent variables and dependent variable is done. Only those variables are kept, those are co-integrated with dependent variable.

- Correlation between independent variables and dependent variable is done. Only those variables are kept, those have high correlation with dependent variable.

- OLS Model is developed

2.3 Independent Variables

| Raw | Diff QoQ | Diff YoY | Pct Diff QoQ | Pct Diff YoY | |

| Lags 0, 1 and 2 | Lags 0, 1 and 2 | Lags 0, 1 and 2 | Lags 0, 1 and 2 | Lags 0, 1 and 2 | |

| GDP growth | Yes | No | No | No | No |

| Income growth | Yes | No | No | No | No |

| CPI growth | Yes | No | No | No | No |

| Unemp rate | Yes | Yes | Yes | No | No |

| 3mT rate | Yes | Yes | Yes | No | No |

| 5yT rate | Yes | Yes | Yes | No | No |

| 10yT rate | Yes | Yes | Yes | No | No |

| BBB rate | Yes | Yes | Yes | No | No |

| Prime rate | Yes | Yes | Yes | No | No |

| HPI | Yes | No | No | Yes | Yes |

2.4 Model Outputs

- Time Period

- Historical – 44 data points (from 2005Q1 to 2015Q4)

- Forecasted – 13 data points (from 2016Q1 to 2019Q1)

- Non-interest Income and Non-interest Expense are modeled

- Non-interest Expense is modeled using the stationary model developed approach

- Non-interest Income is modeled using the non-stationary model developed approach

| Non-interest Expense(Stationary model developed approach) | Non-interest Income(Non-stationary model developed approach) |

|  |

2.5 Model Tests

- Stationarity of dependent and independent variables:

- ADF test is done

- If the p-value <= 0.10 then the series is stationary

- If the p-value > 0.10 then the series is non-stationary

- Multi co-linearity:

- Correlation matrix is used to test multi co-linearity

- If the correlation between variables is less than 0.30 or more than -0.30 then there is low multi co-linearity

- If the correlation between variables is more than 0.70 or less than -0.70 then there is high multi co-linearity

- Significance:

- The p-value <= 0.05 then the coefficient is statistically significant

- The p-value > 0.05 then the coefficient is statistically insignificant

- Auto correlation:

- Durbin-Watson test is done

- If DW statistics is less than 1 then there is positive auto correlation

- If DW statistics is close to 2 then there is no auto correlation

- If DW statistics is more than 3 then there is negative auto correlation

- Stationarity of residual:

- ADF test is done

- If the p-value <= 0.10 then the series is stationary

- If the p-value > 0.10 then the series is non-stationary

3. Stationary Series

3.1 Process

- ADF test is done on the independent variables. Only stationary variables are kept (23 out of 72 variables are selected).

- Correlation between independent variables and dependent variable is done. Only those variables are kept, that have high correlation with dependent variable (2 out of 23 variables are selected).

- OLS Model is developed, checks on multi co-linearity, significance of the variable and stationary of the residuals are done (2 out of 2 variables are selected).

3.2 Dependent Variables

- It is observed that the dependent variables (Non-Interest Income 1st Difference and Non-Interest Expense 1st Difference) are stationary

- Non-Interest Income 1st Diff = Non-Interest Income (t) – Non-Interest Income (t-1)

- Non-Interest Expense 1st Diff = Non-Interest Expense (t) – Non-Interest Expense (t-1)

| Var | ADF | Pval |

| NonInt Inc diff | -5.20 | 0.00 |

| NonInt Exp diff | -5.98 | 0.00 |

3.3 Independent Variables

- It is observed that out of 72 independent variables, 23 independent variables are stationary.

- If the p-value <= 0.10 then the series is stationary

- If the p-value > 0.10 then the series is non-stationary

- It is observed that no macro-economic variable has high correlation with Non-Interest Income 1st Diff. However, few macro-economic variables have high correlation with Non-Interest Expense 1st Diff.

- If correlation is more than 0.30 or less than -0.30 then it is marked as high

- It is observed that out of 23 independent variables, 2 independent variables have high correlation with Non-Interest Expense 1st Diff.

| NonInt Exp diff | |

| CPI growth | 0.31 |

| GDP growth 2 | 0.43 |

3.4 Model Development

- It is observed that the model has low R-Sq and Adj R-Sq.

| No. Obs: | 43.00 | R-squared: | 0.29 | |

| Df Model: | 2.00 | Adj. R-squared: | 0.26 |

- There are 2 variables in the model.

- CPI growth and GDP growth (lag 2)

- The p-value for both the variables is less than 0.05

| coef | std err | t | P>|t| | |

| const | -377,300.00 | 134,000.00 | -2.82 | 0.01 |

| CPI growth | 86,320.00 | 35,500.00 | 2.43 | 0.02 |

| GDP growth 2 | 122,800.00 | 36,600.00 | 3.36 | 0.00 |

- It is observed that there is very low multi co-linearity in the model

- Correlation between variables is less than 0.30 or more than -0.30

| CPI growth | GDP growth 2 | |

| CPI growth | -0.04 | |

| GDP growth 2 | -0.04 |

- It is observed that there is no auto-correlation in the model and the residual is stationary

- DW test statistics is close to 2

- The p-value of the ADF test is less than 0.10

| Durbin-Watson: |

| 2.36 |

| Var: | ADF: | Pval: |

| RESI | -8.30 | 0.00 |

3.5 Projection

- The projection is done for 13 Quarters

- If t = 1: Predicted Non-Interest Expense (t) = Actual Non-Interest Expense (t)

- If t > 1: Predicted Non-Interest Expense (t) = Predicted Non-Interest Expense (t-1) + Predicted Non-Interest Expense 1st Diff (t)

- The severely adverse projection is done for forecasted period

4. Non-stationary Series

4.1 Process

- ADF test is done on the independent variables. Only non-stationary variables are kept (49 out of 72 variables are selected).

- Co-integration between independent variables and dependent variable is done. Only those variables are kept, those are co-integrated with dependent variable (6 out of 49 variables are selected).

- OLS Model is developed, checks on multi co-linearity, significance of the variable and stationary of the residuals are done (1 out of 6 variables is selected).

4.2 Dependent Variables

- It is observed that the dependent variables are non-stationary

| Var | ADF | Pval |

| NonInt Inc | -2.14 | 0.23 |

| NonInt Exp | -1.49 | 0.54 |

4.3 Independent Variables

- It is observed that out of 72 independent variables, 49 independent variables are non-stationary.

- If the p-value <= 0.10 then the series is stationary

- If the p-value > 0.10 then the series is non-stationary

- It is observed that no macro-economic variable is co-integrated with Non-Interest Expense. However, few macro-economic variables are co-integrated with Non-Interest Income.

- If the p-value <= 0.10 then the series is co-integrated

- If the p-value > 0.10 then the series is not co-integrated

| Var | Coint_Inc | Pval_Inc |

| 3mT rate dyoy | -3.37 | 0.05 |

| 3mT rate dyoy 1 | -3.24 | 0.06 |

| 5yT rate dyoy | -3.21 | 0.07 |

| 5yT rate dyoy 1 | -3.38 | 0.04 |

| Prime rate dqoq 2 | -3.39 | 0.04 |

| Prime rate dyoy | -3.31 | 0.05 |

4.4 Model Development

- It is observed that the model has high R-Sq and Adj R-Sq.

| No. Obs: | 44.00 | R-squared: | 0.66 | |

| Df Model: | 1.00 | Adj. R-squared: | 0.65 |

- There is 1 variable in the model.

- 3mT rate (difference YoY)

- The p-value for the variable is less than 0.05

| coef | std err | t | P>|t| | |

| const | 7,656,000.00 | 249,000.00 | 30.80 | 0.00 |

| 3mT rate dyoy | 1,786,000.00 | 199,000.00 | 8.99 | 0.00 |

- It is observed that there is positive auto-correlation in the model and the residual is stationary

- DW test statistics is less than 1

- The p-value of the ADF test is less than 0.10

| Durbin-Watson: |

| 0.85 |

| Var: | ADF: | Pval: |

| RESI | -3.33 | 0.01 |

- Since there is positive auto-correlation in the model, ARIMAX model is developed

- The ACF and PACF plots are generated for the OLS residual

- Based on the ACF and PACF plot, AR(1) model is developed

- Reference: Time Series Modeling and Forecasting—An Application to Bank’s Stress Testing, SAS Global Forum 2015, Paper 3338-2015

- ARIMAX model specifications

- P, D, Q = 1, 0, 0

- X = 3mT rate dyoy

- When AR(2) term was introduced in the model, it was found to be insignificant, hence higher lags for AR are not included in the model

| No. Obs: | 44.00 | AIC | 1,380.03 | |

| Sample: | 0.00 | BIC | 1,375.54 |

- There are 2 variables in the model.

- AR(1) term and 3mT rate (difference YoY)

- The p-value for both the variables is less than 0.05

- The sigma2 in the coefficients table is the estimate of the variance of the error term.

| coef | std err | t | P>|t| | |

| const | 7,656,000.00 | 563,000.00 | 13.59 | 0.00 |

| 3mT rate dyoy | 1,786,000.00 | 264,000.00 | 6.76 | 0.00 |

| ar.L1 | 0.56 | 0.13 | 4.24 | 0.00 |

| sigma2 | 1.75E+12 | 0.17 | 1.05E+13 | 0.00 |

- It is observed that there is no auto-correlation in the model and the residual is stationary

- DW test statistics is close to 2

- The p-value of the ADF test is less than 0.10

| Durbin-Watson: |

| 1.77 |

| Var: | ADF: | Pval: |

| RESI | -5.74 | 0.00 |

4.5 Projection

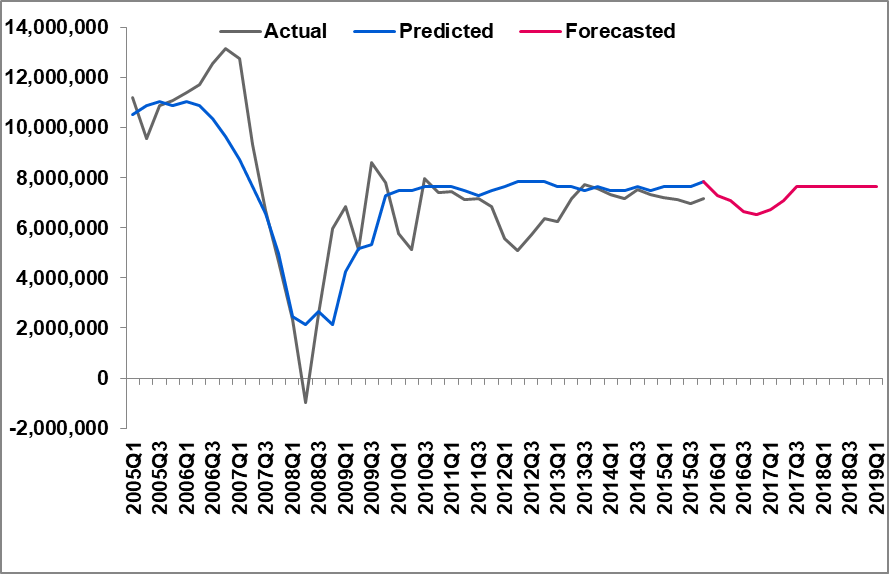

- The projection is done for 13 Quarters

- The dip in 2008-2009 is captured well by the model

- The severely adverse projection is done for forecasted period

- Graph

- Predicted (Blue line) – OLS model

- Forecasted (Red line) – ARIMAX model